Boutique Hotel Acquisition - Villa Castollini

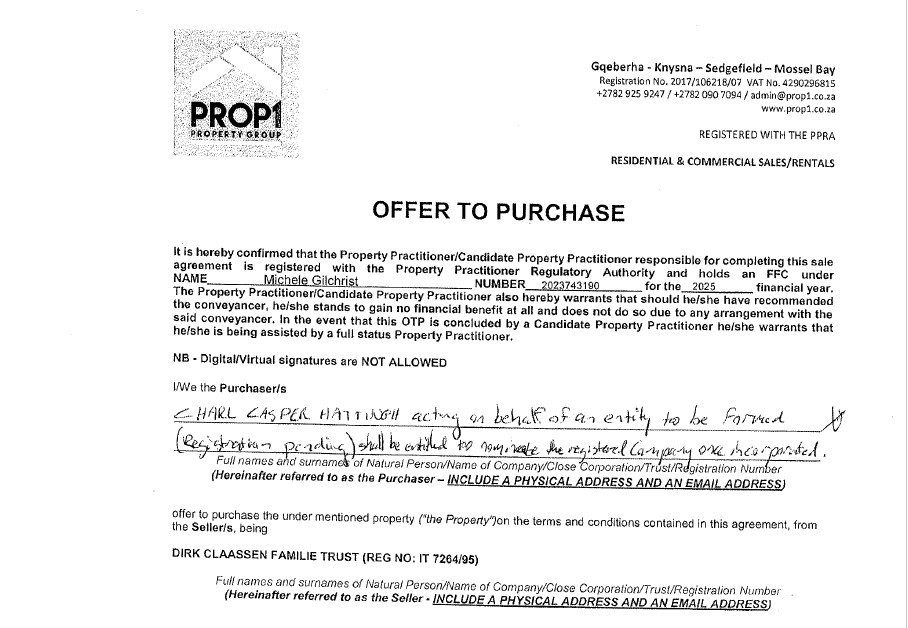

Offer to Purchase

Property valuation summary

Property Valuation Summary – Villa Castollini

Subject Property: Villa Castollini

Location: Brenton-on-Sea, Knysna, Western Cape, South Africa

Property Type: Luxury Villa / Hospitality Asset (Boutique Hotel Conversion Potential)

Zoning: Argricultural Zone I / Hospitality Use Permitted

Erf Size: 20.56 ha

Final Valuation Reconciliation

Income Capitalisation Approach (Affordable rental) Valuation =

R57 000 000

EBITDAR Multiple & Capitalisation of EBITDAR Valuation (Enterprise guideline value for informative purposes only) =

R90 000 000

Depreciated Replacement Cost Approach Valuation =

R58 000 000

Final Property Value =

R58 000 000

All financial statements and supporting documents are available upon request and are strictly confidential. They are intended solely for evaluation by aligned banking partners. No part of this material may be shared, reproduced, or acted upon independently without the express written consent of the Sponsor, Charl Hattingh.

Estimated Market Value (Post-Renovation / Boutique Hotel Conversion)

Assumed Annual Debt Service: R7.43m

Phase / NOI / (R) / Value @10% Cap / DSCR

Year 1 – Stabilisation R13.7m (NOI) R137m (Value) 1.84× (DSCR)

Year 2 – Construction (partial disruption) R12.0m (NOI) R120m (Value) 1.62× (DSCR)

Year 3 – Full Upgrade Online R16.8m (NOI) R168m (Value) 2.26× (DSCR)

Year 4 – Optimisation R18.0m (NOI) R180m (Value) 2.42× (DSCR)

Year 5 – Revaluation R18.5m (NOI) R185m+ (Value) 2.49× (DSCR)

Valuation uplift: ±R40–55m within 24 months

Debt risk trend: Improves every year post-acquisition

Rental / Revenue Potential (Indicative Figures)

Average Daily Rate (ADR): R2,500

Occupancy Potential: 55% – 75% (seasonally adjusted)

Gross Annual Revenue Projection (Stabilized): R8.5M – 11M

SCALABILITY UPSIDE – BOUTIQUE HOTEL CONVERSION

(Equity-funded, not relied upon for debt service)

1. Accommodation Expansion (Room Increase)

Assumption clarity (bank-safe):

Existing “extra rooms” generate R300,000/month

Based on comparable ADR and occupancy

Boutique upgrade allows replication at same yield

Impact:

Existing: R300,000/month = R3.6m/year

Additional rooms (doubling capacity): +R300,000/month

➡ Incremental uplift: +R3.6 million annually

Zabella’s – Upscaled Restaurant & Venue

Current: ±R1.63m/year

Post-upgrade drivers:

Increased seating

Event hosting

Higher foot traffic from increased occupancy

Formal restaurant consent use

Conservative post-upgrade estimate:

R3.6m/year

➡ Incremental uplift: +R2.0 million annually

Tour Group Expansion

Current: R2.0m/year

Drivers:

Increased room inventory

Larger group capacity

Multi-night stays

Post-upgrade conservative: R3.0m/year

Incremental uplift: +R1.0 million annually

Synthetic Ice Rink 3–5 Month Payback and Strong Cash Yield

The synthetic ice rink is not just a standalone revenue stream — it is a demand engine for Villa Castollini.

It introduces a high-energy, family-friendly and experiential attraction that materially increases foot traffic, dwell time, and repeat visitation to the property.

From a financial perspective, the capital outlay of approximately R2.3 million is recovered quickly through direct ticket sales, after which the rink becomes a strong cash generator. More importantly, every skating session drives incremental restaurant covers, beverage sales, events, and private bookings, turning the rink into a feeder for the core hospitality business rather than a distraction from it.

The experience naturally extends guest stay duration, converts visitors into diners, and positions Villa Castollini as a destination rather than just a restaurant or venue. In effect, the rink enhances hospitality revenue per guest while creating an additional income line that is low-risk, low-utility, and highly complementary to the brand.

I’d welcome the opportunity for you to review the full business plan, which details the capital structure, payback mechanics, and the broader hospitality uplift this asset creates for Villa Castollini.

TOTAL POST-UPGRADE GROSS INCOME (CONSERVATIVE)

Category / Annual (R)

Base Stabilised Income 12,129,000

Accommodation Expansion +3,600,000

Zabella’s Upscale +2,000,000

Tour Group Expansion+1,000,000

Synthetic ICE Rink +6,390,000

A 400 m² modular synthetic ice rink delivering fast capital recovery, low operating risk, and repeatable returns — without refrigeration, heavy utilities, or seasonal dependency.

Total Post-Upgrade Gross R20M+

Rounded: ±R19.0 million

This intentionally excludes:

Brand affiliation upside

Full boutique ADR uplift

Venue/event upside beyond conservative assumptions

Which is why R20m+ is achievable but not overstated

SUMMARY

a Structurally sound, prime-located hospitality property with the potential to evolve from a private villa, to a boutique hotel, and ultimately into a full destination resort

CURRENT PERFORMANCE –

WHY IT’S UNDERPERFORMING:

This is not a reflection of asset quality, but of its current value-add phase—precisely the dislocation that creates institutional upside. With modest operational optimisation (no heavy construction), the asset can be repositioned from a ~R4m NOI profile to a R20m+ revenue, boutique-hotel platform, supported by existing zoning, conversion plans (30 keys), and multiple under-monetised revenue verticals (rooms, F&B, touring, events, retail, student accommodation etc)

Personal Statement of Assets & Liabilities

With regard to the Personal Statement of Assets & Liabilities, I’d like to respectfully clarify that this transaction is not structured around individual guarantees or personal wealth disclosures. Instead, the strength of this deal lies in the viability of the project itself and the capitalization of the purchasing entity, which will secure funds in escrow within the next 30 days.

While some of the stakeholders and asset positions involved are international—and thus not easily consolidated for local compliance formats—I’m happy to provide a summary-level financial position if required strictly for internal risk profiling.

Ultimately, the transaction stands firmly on its own merits, and the capital is being deployed at the entity level, with all compliance-ready documentation available for your internal review.

I remain fully cooperative should further clarifications be required.

ASSETS

Category

Description

Real Estate Holdings (Hospitality property – New Zealand – income-producing asset)

R20M

Vehicles

R1.5M

Savings & Cash Reserves (liquidity)

R6M

Investments / Business Equity

R10M

Other Assets (IP, valuables, equipment)

R2M

LIABILITIES

Category

Description

Mortgages / Bonds

R4M

Business / Personal Loans

R0M

Other Liabilities (Credit, tax, etc.)

R0

Snapshot

Category

Amount

Total Assets

R39,500,000

Total Liabilities

R3,900,000

Net Worth

R35,600,000

Confirmation of the entity (company docs) in which the funding is to be considered.

I hereby confirm that, pending confirmation of facility approval, the transaction for the acquisition of Villa Castollini will be executed through a newly registered legal entity structured specifically for this project.

The entity will be a (Pty) Ltd, owned and managed under my direction, with the sole purpose of acquiring, upgrading, and operating the subject property.

Registration of this company will be actioned immediately upon receiving a formal funding proposal or approval in principle from funding Institute, and all statutory documentation (company registration, shareholding, director resolution, and loan acceptance resolution) will be submitted accordingly.

This approach ensures that the funding is ring-fenced, operationally focused, and fully compliant with the bank’s requirements once the facility is in place.

Sincerely,

Charl Hattingh

Source of Own Contribution – Statement

The equity contribution will be secured in escrow within 30 days, under the control of the purchasing entity and ready for release upon transfer. Funds are verified, compliant, and we can provide a formal escrow statement or summary confirmation for internal review. We are open to further compliance steps if required, but respectfully ask that stakeholder confidentiality be preserved throughout your internal processes.

Founder & Strategic Lead – HubHubGo

South Africa & Remote | 2020–Present

As Founder of HubHubGo, I oversee a consultancy specializing in analysis, underwriting, and optimization of hospitality, multifamily, and value-add real estate assets. My focus spans underwriting pro formas, enhancing NOI through operational upgrades, and structuring partnerships that deliver scalable returns. Below is a snapshot of how we drive equity through strategic property repositioning.

Strategic Property Underwriting & Asset Review

Developed and refined property underwriting models for clients to evaluate cash flow sensitivity, cap rate scenarios, and value-add tactics—grounding investment assumptions in realistic market comps and risk-adjusted projections.

Designed interactive underwriting tools to stress-test variables such as rent growth, expense reduction, capex timing, financing structures, and hold periods—enabling clients to make data-driven decisions.

Asset Optimization Examples & Operational Enhancements

High-ROI Utility Upgrades: Conducted detailed modeling of utility-based improvements across portfolios—such as low-flow toilets or LED retrofits—demonstrating cost savings that translate into appraised value increases at market cap rates.

Interior Value-Add Projects: Structured interior upgrades (unit refurbs, amenity enhancements, marketing-ready staging) to justify rent increases and improve tenant retention, backed by market comps and lease-up estimates.

Capital Structuring & Strategic Partnerships

Collaborated with early-stage investors, advisors, and developers to craft joint venture structures—covering deal evaluation, cap table setup, investor deck preparation, and equity return modeling.

Assembled cross-functional advisory teams including property managers, real estate attorneys, and local market experts to validate underwriting assumptions and implement on-site initiatives.

Proven Systems for Increasing NOI & Property Value

Perform in-depth underwriting review with supporting market data.

Identify and implement cost-saving upgrades and operational efficiencies.

Execute interior renovations or structural improvements to drive rent growth.

Regularly update pro forma performance, track variance, and refine strategy.

Plan for refinancing or exit strategies to return capital and preserve investor equity.

Why This Experience Matters

This role reflects an advanced understanding of commercial real estate dynamics, including detailed underwriting, capital structure, and value-enhancing renovations. It positions me not only as a strategist but as an implementer who builds cross-functional systems that elevate asset performance, stabilize cash flow, and unlock equity through smart enhancements.

Joint Venture Partner to New Zealand Manuka Group & Northern Life

New Zealand | 2015 – 2020

As Co-Founder and Director of NZM Northlands, I Joint Venture New Zealand’s second-largest independent Manuka honey operation — but more critically, I spearheaded the development, acquisition, and operational management of residential and agricultural real estate assets tied to the business. This included workforce housing, strategic land use agreements, and value-driven infrastructure investments across rural and semi-rural zones.

This experience uniquely positioned me to optimize real estate assets from both an operational and investment standpoint — applying principles of cashflow generation, cost control, and capital appreciation.

Key Real Estate & Operational Achievements

Workforce Housing Development & Management

Designed and managed multiple on-site multifamily housing units to accommodate seasonal and permanent staff (30–50 occupants), ensuring compliance with local housing codes and long-term livability.

Oversaw procurement, maintenance, and capital improvements of units, including insulation, energy-saving utilities, and space efficiency enhancements.

Negotiated short-term and long-term lease structures with flexibility built in for seasonal labor cycles — increasing operational agility and reducing downtime.

Joint Venture Structuring & Asset Partnerships

Co-led structuring of the land-use partnership with New Zealand Manuka Group & Northern Life, aligning operational outputs with real estate control and investment upside.

Negotiated access and stewardship rights on large tracts of native land, enabling shared use without full acquisition — a model that unlocked profitability without heavy capital outlay.

CapEx Deployment & NOI Focus

Implemented infrastructure upgrades (power, water, septic, security) that directly improved asset value and functionality.

Managed budgets and cashflow modeling to determine the ROI of real estate enhancements vs. lease increases and operational savings.

Applied value-add principles to housing and land use — improving livability, efficiency, and asset attractiveness.

Strategic Asset Use & Logistics Integration

Coordinated real estate use between production, housing, and logistics — aligning operations for smoother distribution and workforce flow.

Developed site plans and layouts that reduced transport costs, improved access to hives and export zones, and supported scalability.

This role solidified my ability to create value through both physical real estate and operational systems — a foundation that now informs my current work in hospitality, and value-add investing. It also demonstrates experience working within joint ventures, layered asset structures, and rural regulatory frameworks — key skills when repositioning property assets for higher yield.

2IC to CEO – Jetts Fitness NZ (Franchise HQ, Multi-Site Operations)

New Zealand | 2013 – 2015

As second-in-command to the CEO, I played a pivotal role in maximizing profitability, optimizing operations, and driving revenue growth across a national portfolio of fitness properties. My focus was not just on memberships, but on increasing asset-level performance through operational efficiencies, cost reduction, and strategic upgrades — many of which mirror the same value-add principles I now apply in multifamily and hospitality.

Key Achievements:

Asset Optimization & Repositioning

Identified underperforming clubs and implemented targeted operational upgrades (lighting, water efficiency, HVAC scheduling, etc.), resulting in measurable reductions in overhead and improved EBITDA.

Managed reconfigurations of club layouts to increase usable space, member flow, and secondary revenue opportunities (e.g., vending, group sessions, leasebacks).

Cost Reduction & NOI Growth

Standardized utilities and maintenance contracts across 50+ locations to reduce variability and unlock volume pricing — boosting NOI and stabilizing operations.

Introduced preventative maintenance and vendor scheduling systems that cut reactive repair costs by over 30%.

Revenue Maximization & Space Yield

Leveraged data to analyze space utilization and implemented strategies to increase revenue per square meter, including subleasing unused office/storage space and offering high-yield personal training zones.

Helped reposition select locations by enhancing curb appeal and member experience — directly contributing to membership growth and improved lease renegotiation leverage.

Franchise Support & Expansion Strategy

Led onboarding and operational training for new franchisees, including cost-per-member models, lease reviews, and cashflow optimization.

Supported site selection and landlord negotiations for new locations, contributing to sustainable footprint growth across the country.

Value-Add Insight: Real Savings, Real Equity Growth

Strategic, cashflow-positive repositioning — targeting underperforming properties and unlocking hidden value through operational and utility-based upgrades that directly impact Net Operating Income (NOI) and increase asset value.

Example: Utility Optimization Through Low-Flow Toilet Replacement

Property: 128 Units (Bathrooms)

Upgrade: Replacing 3.5-gallon toilets with 1.28-gallon high-efficiency models

Cost: $28,800

Water Bill per Unit: $65/month

Toilet usage = 26% of total water bill

Savings from low-flow toilets: 64%Annual Toilet Water Savings: $16,613

Value Created at 7% Cap Rate: $237,333

A relatively minor $28,800 investment unlocks over $237,000 in increased appraised value — and this is just one of many simple, high-ROI improvements in Charl's playbook. These kinds of enhancements not only improve the property's performance but also de-risk the investment by increasing cash flow and equity.